This project presents a detailed time series analysis of selected stock price data using Python. The notebook explores temporal patterns, stationarity, decomposition, and smoothing techniques to uncover insights that support forecasting and investment decisions.

- Problem Statement: Understand and model the behavior of stock prices over time to identify trends, seasonality, and volatility.

- Objectives: Apply time series techniques to visualize, decompose, and smooth stock price data for actionable insights.

- Data Source: Historical stock price data retrieved from Yahoo Finance using

yfinance. - Context: Time series analysis is vital in financial modeling, risk management, and algorithmic trading. This project demonstrates intermediate-level techniques for exploring stock dynamics.

- Loading: Stock data is loaded and organized into a pivot table.

- Cleaning: Missing values are handled, and date formats are standardized.

- Validation: Data ranges and completeness are verified across all selected stocks.

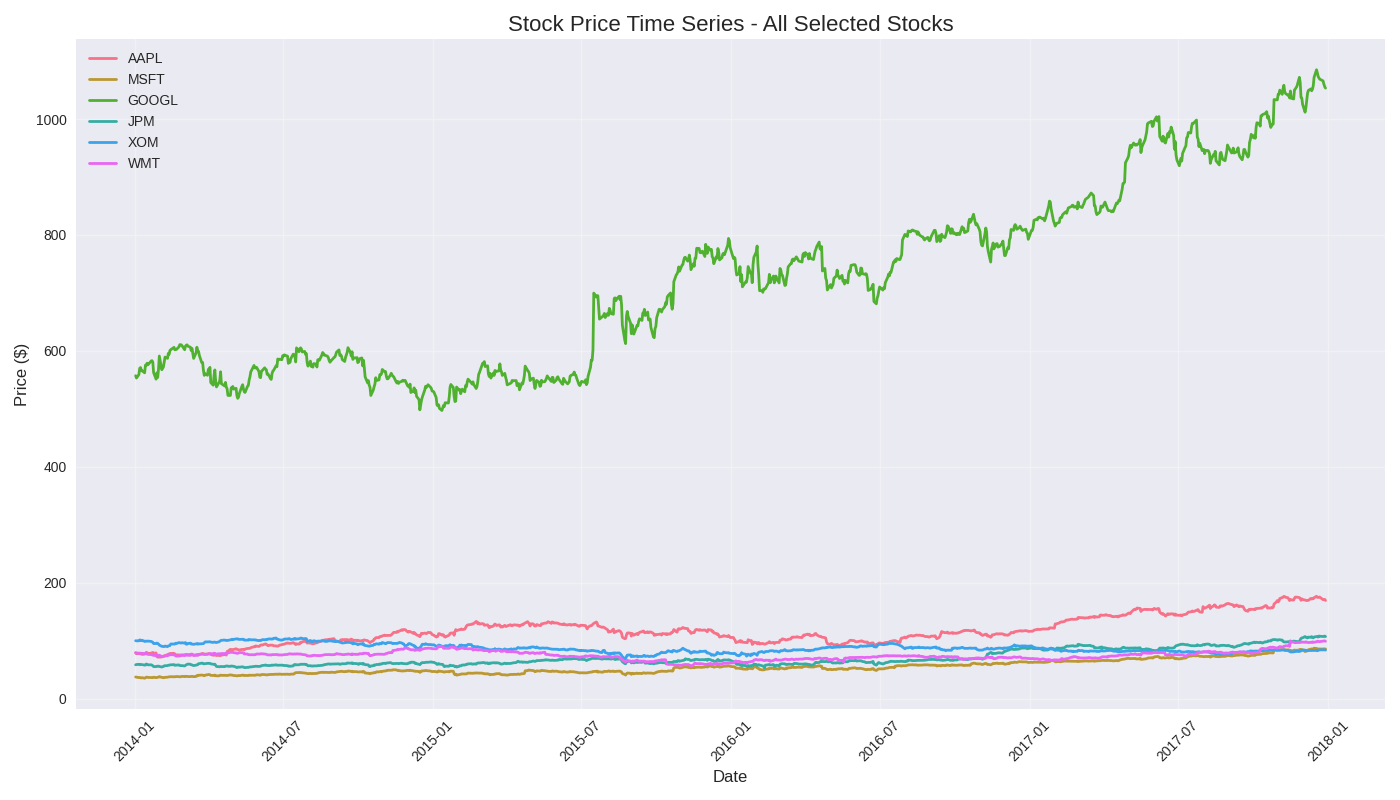

- Visualizations: Individual and comparative time series plots are generated for each stock.

- Statistics: Summary metrics such as mean, variance, and price range are computed.

- Patterns: Initial trends and cyclical behaviors are identified visually.

- ADF Test: Augmented Dickey-Fuller test is applied to assess stationarity.

- Visual Checks: Rolling mean and standard deviation plots are used to support statistical findings.

- Transformations: Log transformations or differencing are suggested if non-stationarity is detected.

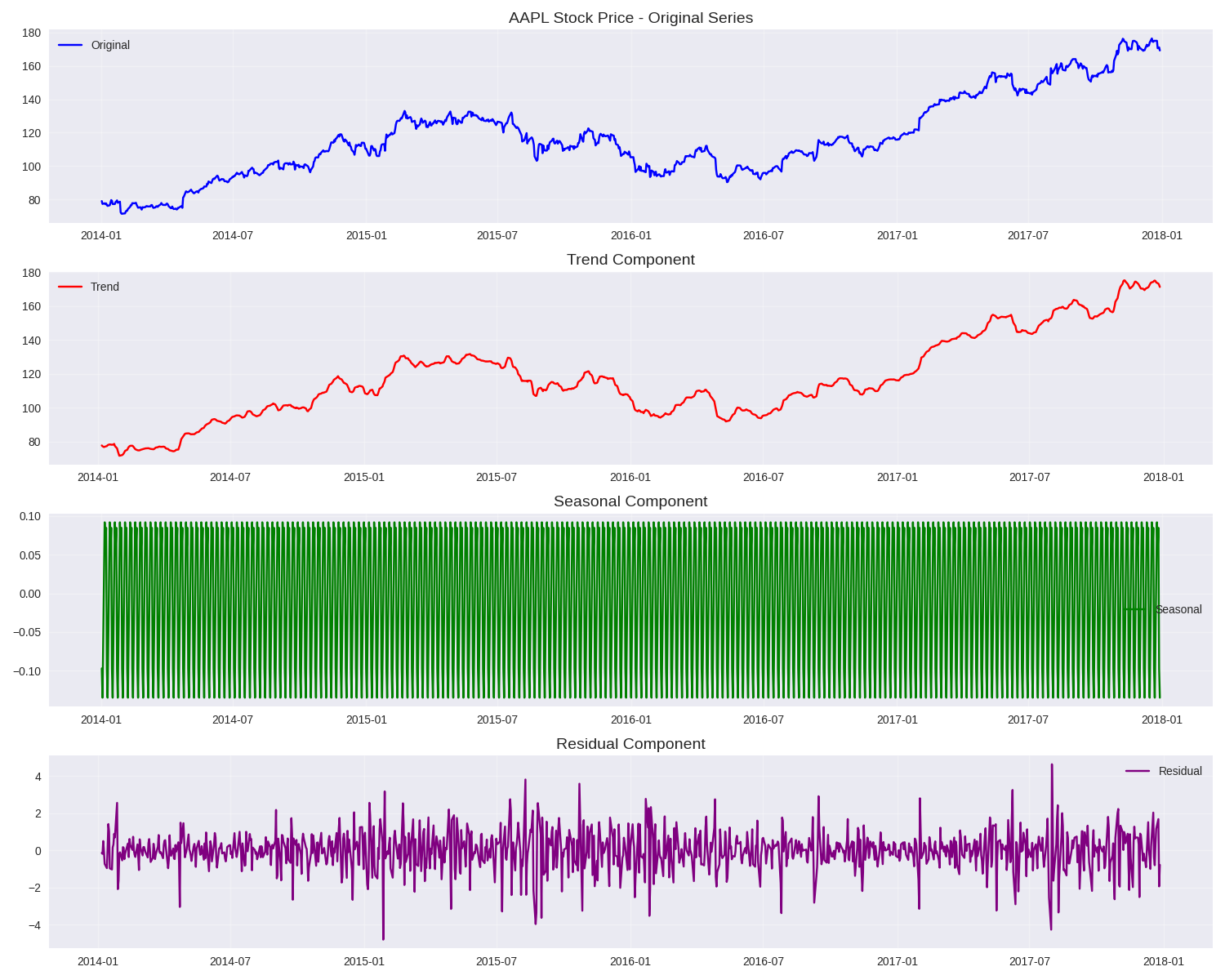

- Method:

seasonal_decomposefromstatsmodelsis used to split the series into:- Trend

- Seasonality

- Residuals

- Model Rationale: Additive decomposition is chosen based on data characteristics.

- Interpretation: Each component is analyzed to understand its contribution to overall price movement.

- Autocorrelation: ACF and PACF plots are used to study lag dependencies.

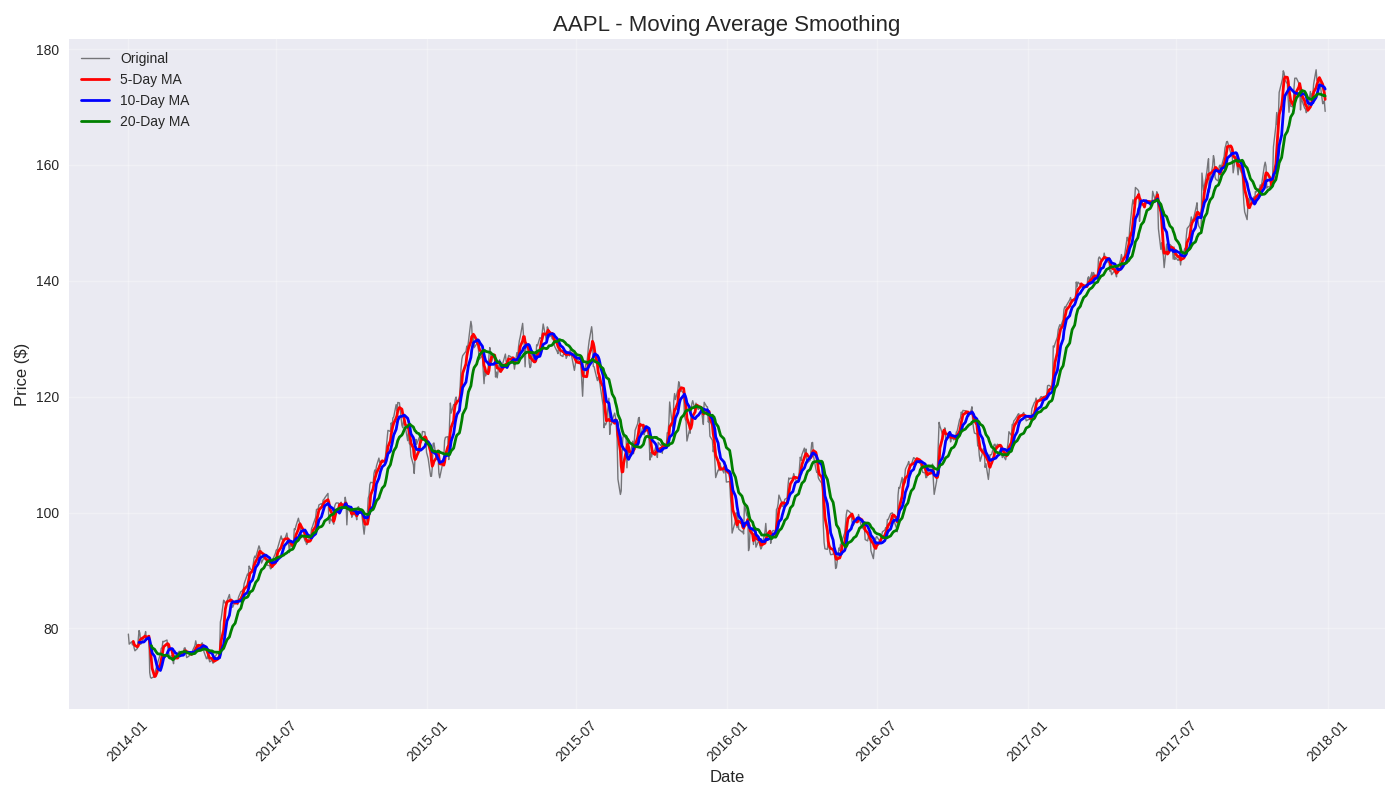

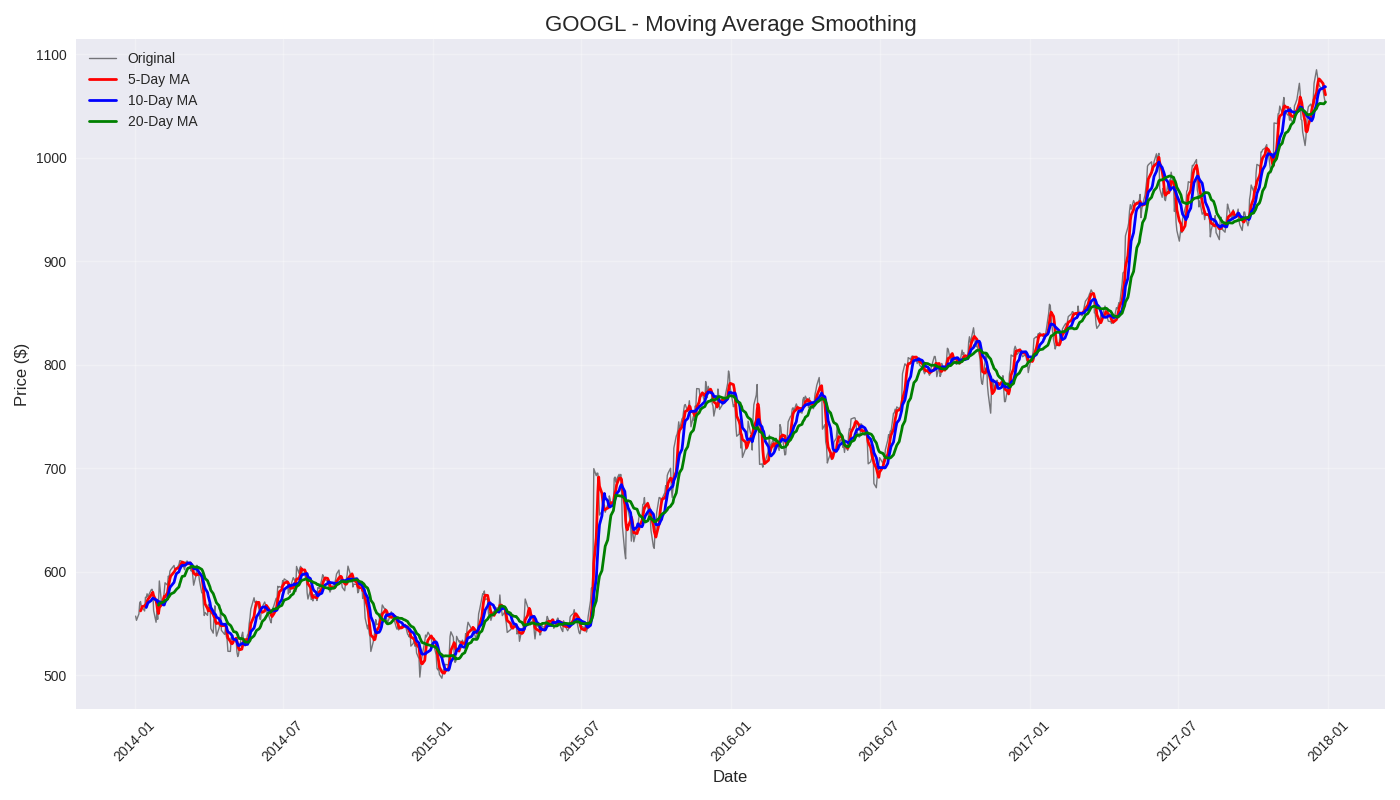

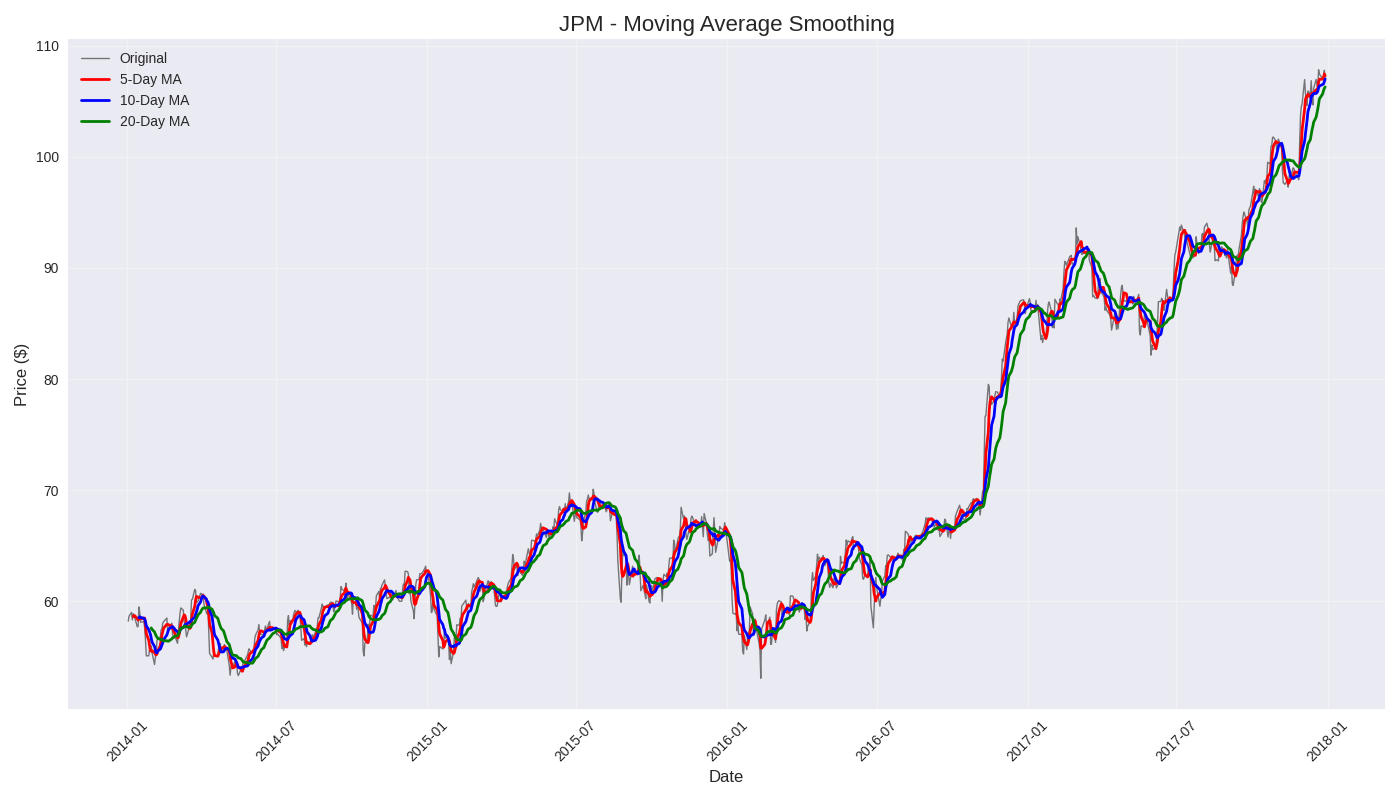

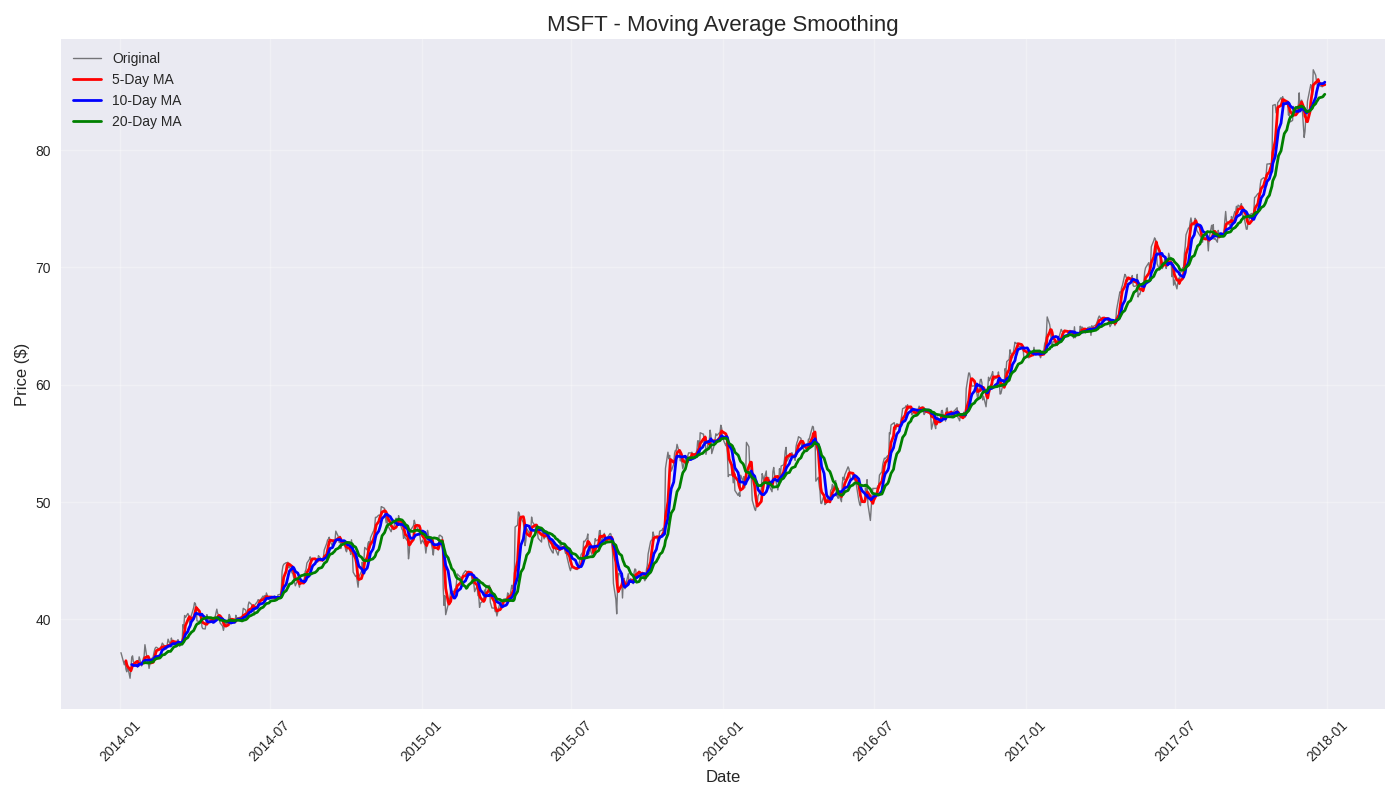

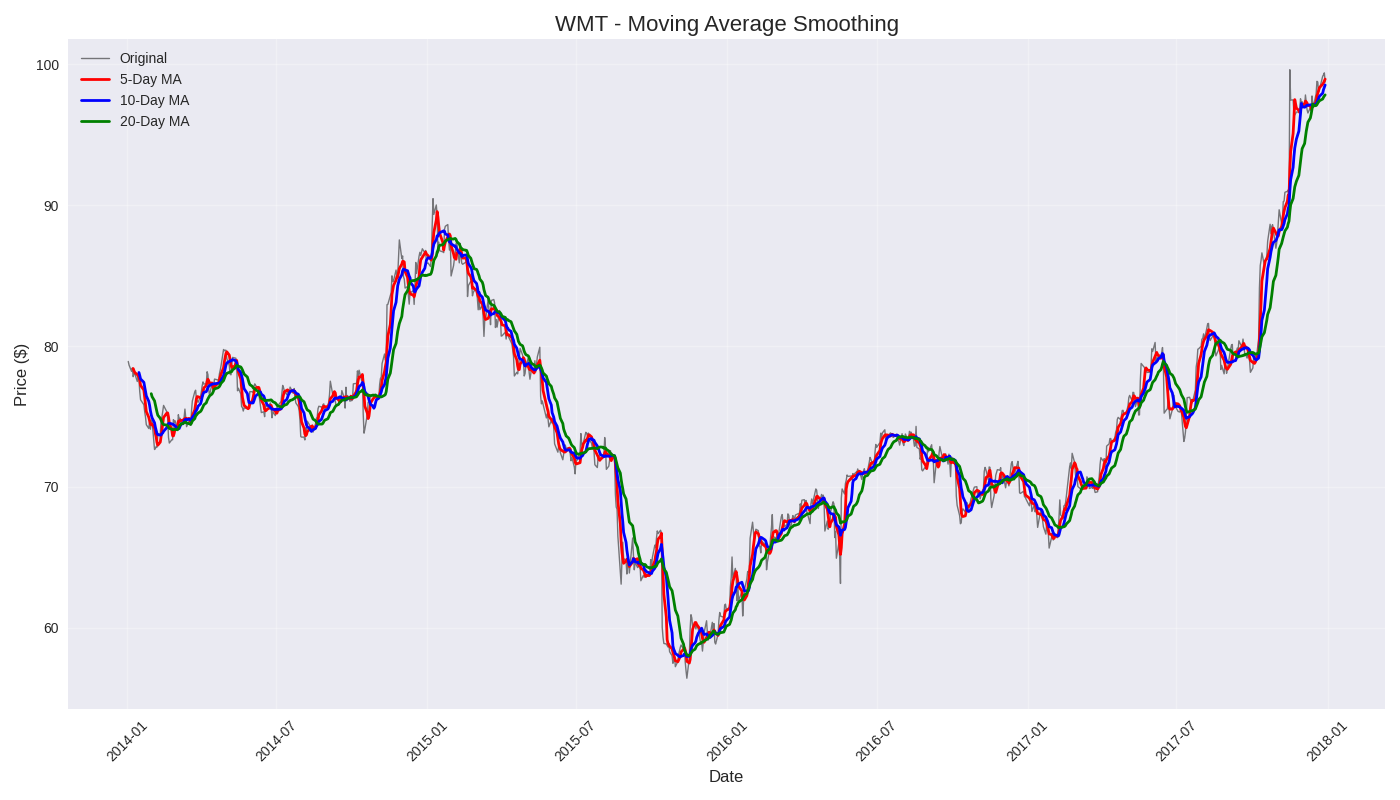

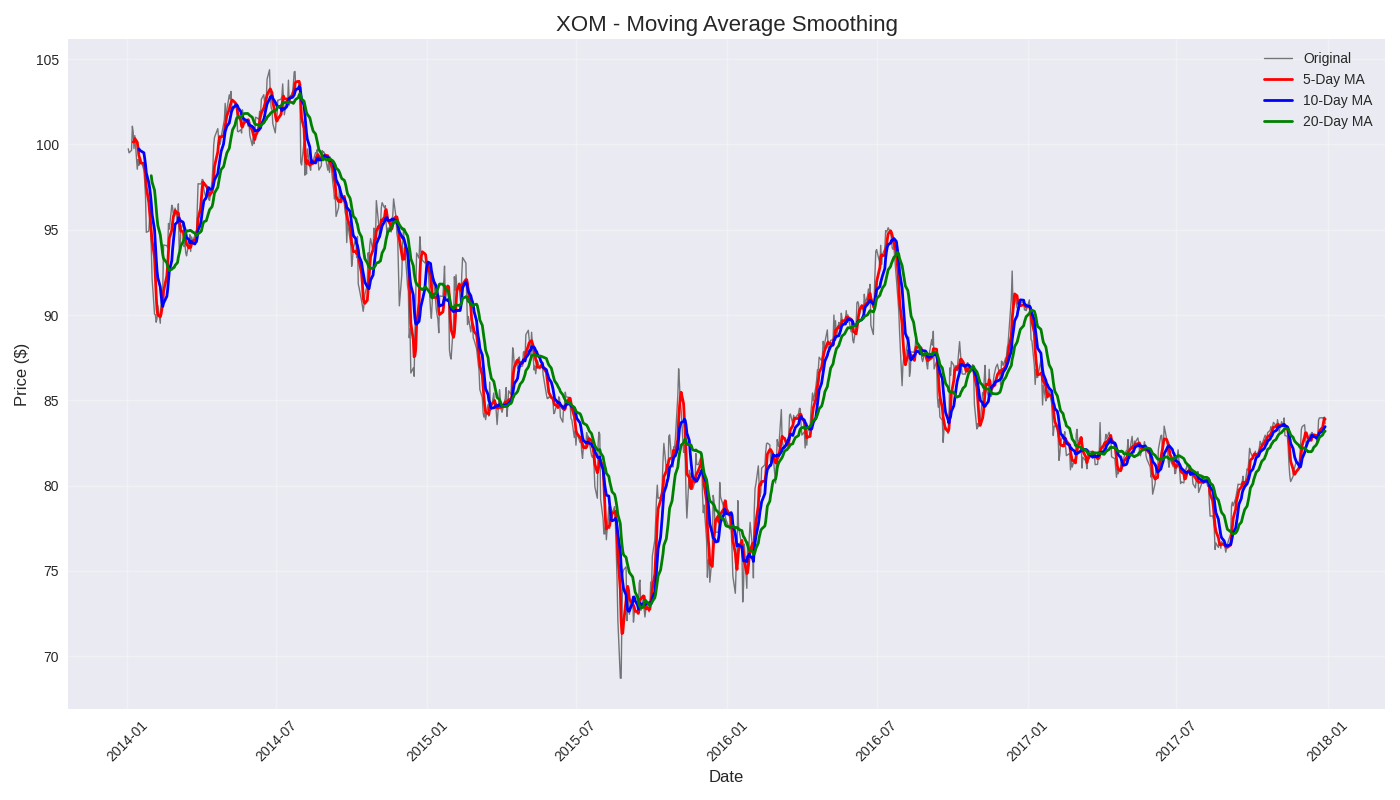

- Moving Average: 30-day smoothing is applied to highlight long-term trends.

- Seasonal Detection: Repeating patterns are examined across months and quarters.

- Investment Insights: Trend analysis supports timing decisions for entry and exit.

- Forecasting: Decomposition and stationarity checks lay the groundwork for ARIMA or Prophet models.

- Risk Management: Understanding volatility and residual noise helps assess uncertainty.

- Key Findings:

- Clear upward trends in selected stocks

- Seasonal dips and spikes aligned with market cycles

- Moderate residual noise indicating partial predictability

- Limitations:

- No forecasting model implemented yet

- Sentiment analysis not fully integrated

- Recommendations:

- Extend with ARIMA or Prophet for forecasting

- Integrate sentiment scores from news headlines or social media

- Build an interactive dashboard for stakeholder presentation

# Clone the repository

git clone https://github.com/Eric-Inkoom-Ayitey/Time-Series-Analysis.git

cd Time-Series-Analysis

# Install dependencies

pip install pandas matplotlib statsmodels yfinance

# Launch the notebook

jupyter notebook Time_Series_Analysis.ipynb